would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

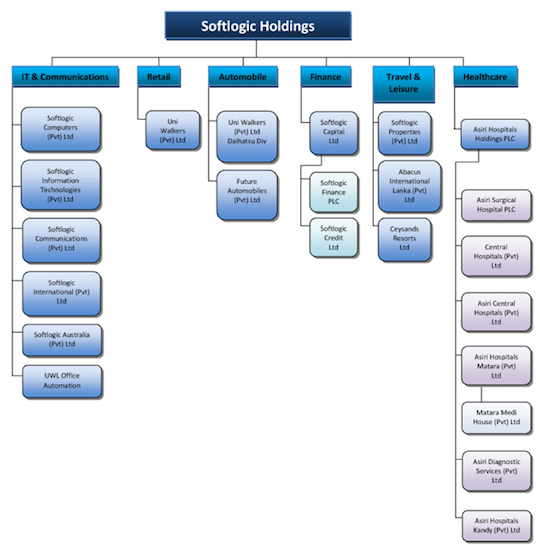

Softlogic private investors to gain over 300% capital gain after IPO

http://www.asiantribune.com/news/2011/05/25/sri-lanka-softlogic-private-investors-gain-over-300-capital-gain-after-ipo

Any Comments....

http://www.asiantribune.com/news/2011/05/25/sri-lanka-softlogic-private-investors-gain-over-300-capital-gain-after-ipo

Any Comments....