would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

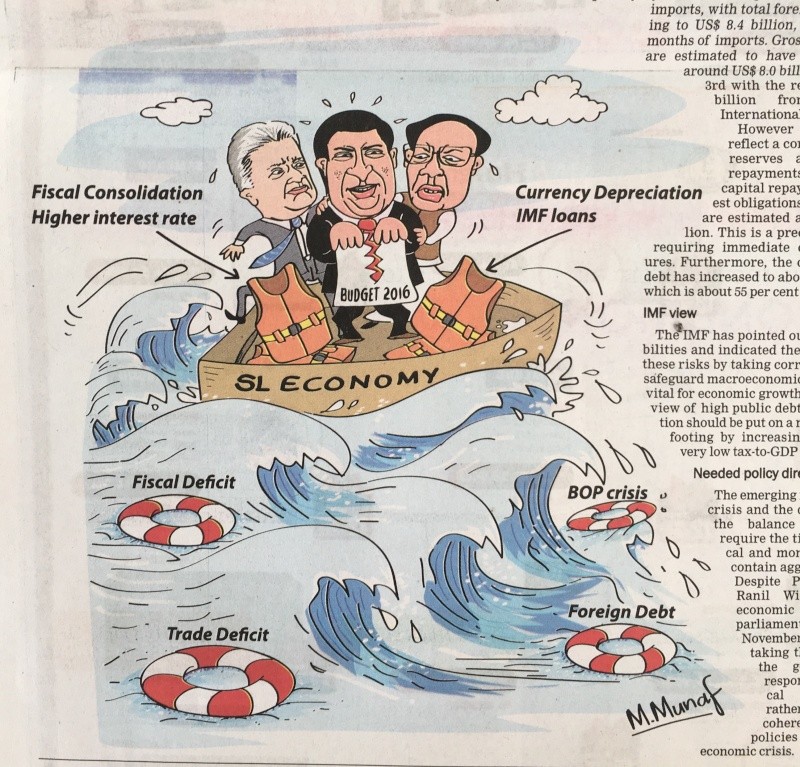

Bold pragmatic policy initiatives are needed to resolve the current economic crisis. However, the policies of the government have not shown adequate sensitivity or response to the developing crisis. The public, trade unions and interest groups are clamouring for more benefits that would aggravate the crisis.

The postponement of remedial actions owing to their unpopularity, ideological differences and divergent political agenda of coalition partners and the opposition, would compound the fiscal, public debt, trade and balance of payments problems.

Crisis

The emerging crisis includes the widening fiscal deficit that is increasing domestic and foreign debt that is already at an unsustainable level and increasing the trade deficit that is causing balance of payments difficulties. These together with repayment of foreign debt obligations and outflow of foreign investment funds have eroded foreign reserves to a dangerous level.

These macro economic conditions would destabilise the economy. Remedial fiscal, monetary, external trade and financial policies must be adopted, sooner rather than later, to resolve these economic imbalances to ensure macroeconomic stability.

Budget aggravates

The recent budget and post budget changes have not addressed these problems adequately. Further changes in the budget could compound not only the fiscal problem, but intensify the debt and balance of payments problems as well. The inability to contain the fiscal deficit and aggregate demand is increasing the trade deficit and straining the balance of payments that is in dire straits in a context of inadequate and declining foreign reserves.

Fiscal deficit

The fiscal deficit in the original budget was itself too high at six per cent of GDP. The inadequate and uncertain taxation measures made the realisation of even this target unrealistic. Economists and tax experts have expressed doubts that revenue would be increased by as much as expected in 2016. Several changes already announced and likely to be made would reduce revenue, on the one hand, and increase expenditure on the other. These would aggravate the fiscal problem that is the fundamental flaw in the economy that deteriorates the trade and balance of payments problems.

The thrust of post budget changes have been in the wrong direction of reducing revenue and enhancing government expenditure that would increase the fiscal deficit. If countervailing measures are not taken the fiscal deficit could balloon to seven per cent or more of GDP.

Systematic tax system

A more systematic progressive taxation system that would increase revenue by eliminating tax exemptions reduces tax avoidance and tax evasion is needed. Admittedly a rigorous tax administration is essential to increase the country’s tax revenues from its very low tax to GDP ratio. This is a serious deficiency that cannot be corrected easily in the short term.

Trade deficit

The trade deficit is likely to exceed US$ 8.5 billion this year compared to last year’s large deficit of US$ 8.3 billion. In the first nine months of this year, the trade deficit increased to reach US$ 6.1 billion compared to US$ 5.9 billion in the first nine months of last year. This was despite the advantage of much lower international oil prices and a lesser demand of fuel for the generation of electricity owing to higher hydro electricity generation enabled by heavy rains. Consequently imports of oil decreased by as much as 46 per cent.

Unfortunately this advantage was frittered away by increased consumer imports owing to mismanagement of fiscal and monetary policies that enhanced aggregate demand that resulted in higher imports of consumer durables. Consequently total imports decreased by only 0.6 per cent mainly due to consumer imports increasing by 33 per cent with vehicle imports increasing by as much as 79 per cent.

Attempting to close the stable door even after the horses have bolted appears to be failing. Even in September this year consumer imports increased by 7.4 per cent with vehicle imports increasing by 30 percent compared to that of September 2014.

The trade deficit of US$ 6.1 billion in the first nine months of the year projects a trade deficit of over US$ 8.5 billion unless the depreciation of the rupee curtails imports significantly.

Balance of payments

The balance of payments registered a deficit of US$ 4.2 billion in the first nine months of this year, compared to a surplus of US$ 2 billion in the same period last year. This deterioration in the balance of payments by US$ 6 billion is indicative of the serious balance of payments problem the country is facing.

Increases in tourist earnings and remittances have been favourable aspects of the balance of payments. Tourist earnings increased by 18.8 per cent to US$ 2.1 billion in the first ten months. Despite the unsettled conditions in the Middle East, from where about 55 per cent of remittances originate, remittances have increased by 1.8 per cent to US$ 5.2 billion in the first ten months of the year. On the other hand there has been a net outflow of investment funds

External reserves and debt

External reserves are at a dangerous level. According to the Central Bank, the country’s gross official reserves were at US$ 6.8 billion as at end September this year that was equivalent to 4.2 months of imports, with total foreign assets amounting to US$ 8.4 billion, equivalent to 5.2 months of imports. Gross official reserves are estimated to have strengthened to around US$ 8.0 billion by November 3rd with the receipt of US$ 1.5 billion from the ninth International Sovereign Bond.

However this does not reflect a comfortable level of reserves as foreign loan repayments that consist of capital repayments and interest obligations for the next year are estimated at over US$ 4 billion. This is a precarious situation requiring immediate corrective measures. Furthermore, the country’s foreign debt has increased to above US$ 44 billion, which is about 55 per cent of GDP.

IMF view

The IMF has pointed out these vulnerabilities and indicated the need to contain these risks by taking corrective actions to safeguard macroeconomic stability that is vital for economic growth. It urges that in view of high public debt, the fiscal position should be put on a more sustainable footing by increasing the country’s very low tax-to-GDP ratio.

Needed policy directions

The emerging macro economic crisis and the deterioration in the balance of payments require the tightening of fiscal and monetary policy to contain aggregate demand. Despite Prime Minister Ranil Wickremesinghe’s economic statement to parliament in early November that advocated taking the “bitter pill”, the government is responding to political compulsions rather than following coherent economic policies to resolve the economic crisis.