would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

The global economy is in turmoil. Future economic prospects seem to be rather bleak in the midst of geo political tensions, terrorism, low levels of production (e.g. China), unsustainable debt, upward trend in interest rates(U.S.A. increasing rates by 0.25 percent in December) and decreasing prices of key commodities. As a country that is integrated with the global village the impact of these conditions are strongly felt within our nation. The winds of global economic slowdown makes it increasingly difficult to combat the economic problems deep rooted within the Sri Lankan economic and political structure. An unsustainable level of debt is one such dilemma.

Debt is a burning issue

The previous regime provided impetus towards economic growth by increasing government expenditure through debt financing. As a result, government debt has exceeded manageable limits. According to the latest documents, the country’s total outstanding loans at the end of year 2015 were Rs.8,475 billion, which amounts to 74.9 percent of the gross domestic product (GDP). The country is in a horrendous debt trap of Rs.9.5 trillion.

Even though increasing demand through government expenditure is a widely accepted economic policy centralizing such policies around unsustainable levels of debt is inappropriate. As a result, the country is currently faced with a debt trap.

The way forward

On one hand, the government has to manage the debt trap and on the other hand it has to manage the impact of the global economic slowdown. The current predicament compels the government to take up stringent measures in relation to fiscal and monetary policy. Accordingly, increasing tax revenue becomes a feasible fiscal tool.

Prime Minister Ranil Wickremesinghe adopted the aforesaid approach by making proposals to the parliament to change certain taxes. Principal among these changes is the reintroduction of capital gains tax, increasing the rate of Value Added Tax (VAT), removing certain exemption on VAT and Nation Building Tax (NBT) and thereby widening the tax base.

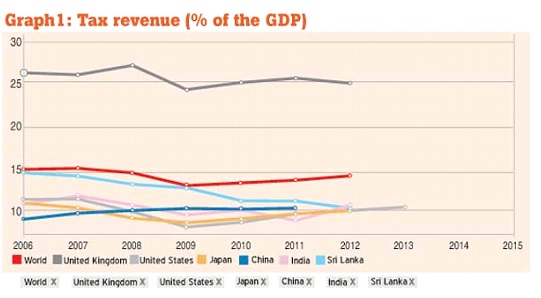

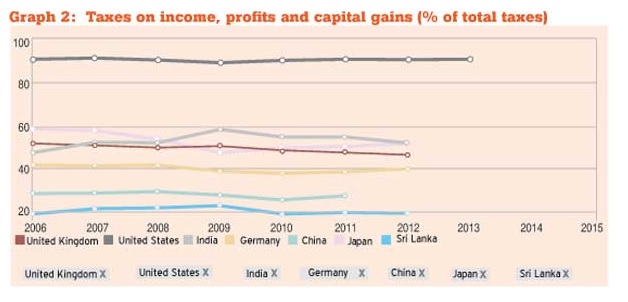

Historical data reveals that tax revenue as percent of the GDP has not only been below 15 percent but also recorded a declining trend (refer graph 1) since 2006. Further on taxes on income, profits and capital gains (percent of total taxes) has also been relatively low when compared to its counterparts(graph 2). One would argue that the structural deficiencies in tax collection/tax structure and popular politics can be attributed to low tax levels. Employing this fiscal tool is long overdue. Nevertheless, its appropriateness within the current context is questionable.

Capital Gains Tax

It has been proposed to reintroduce tax on capital gains. A capital gains tax is a type of tax levied on capital gains incurred by individuals and corporations. Capital gains are the profits that an investor realizes when he or she sells the capital asset for a price that is higher than the purchase price. An investor can own shares that appreciate every year, but the investor does not incur a capital gains tax on the shares until they are sold. It was proposed to introduce this tax for capital gains generated in the stock market. This could be explained further through an example. Imagine that you purchased 1000 shares at Rs.2 from the market. After one year you sell the share at Rs.3.Then your capital gain will be Rs.1000.According to the proposed amendment a tax will be levied on the capital gain of Rs.1000.

The capital gain tax would have a direct impact on the market. The market has decreased by more than 10 percent for the current year. The current trend is in line with global equity prices that have plunged down drastically. For an example, the Chinese stock market has decreased by 24percent this year. Nevertheless the local equity market has managed to sustain a satisfactory performance in comparison to its counterparts. However, it is reasonable to question if these commendable levels will continue amidst the tax amendment. Investment decision-making is well grounded on expected returns. Tax of this nature would reduce expected returns and investors would be compelled to look at other avenues amidst rising interest rates.

Benjamin Graham in his book ‘The Intelligent Investor’ states that investing in the market is more about emotion than intelligence. Hence, introducing this tax within the current market condition might falter investor confidence and create undue resistance towards equity. Situation might aggravate due to the herd mentality in the market.

Could direct taxes hinder growth?

The country is currently burdened with debt. In such an environment a government is faced with a few options. They could increase tax revenue, encourage FDIs or enter into more debt to repay of the current debt. It is well established that the latter is inappropriate and thereby we are left with the first two options.

Direct taxes (e.g. capital gain tax) reduce the real income of households. This would hamper consumption and thereby reduce aggregate demand in the economy which is a key driver of economic growth. Slowdown in growth will worsen the debt situation.

Ease of doing business, conducive tax structure and political/economic stability will be the manthra to attract FDIs. A tax that hampers profits will definitely compel investors to look at competitors as India, China, Vietnam, etc. The same principle would apply for portfolio investments. The government is indeed faced with a double edged sword. On the one hand it is exploring the opportunities of attracting FDIs and on the other hand might fail to foster a suitable environment for investment. It is rational to postulate the returns on tax revenue in comparison to the loss of foreign investment.

Clearing the air

There are a few decisive factors that would determine the impact of this tax especially in the context of the stock market. The tax structure has not been revealed as yet. The industry is optimistic that it will be between manageable limits. Further on the responsiveness of the capital gains tax to investment decision (in the stock market) is another crucial point to ponder on. It is important to bear in mind that market performance is influenced by many factors. Accordingly capital gain tax is a one factor among a myriad of other vital factors.

It could be postulated that the tax might not have a considerable impact on the market if all other factors are in place. This is clearly manifested in the abolition of the Government levy by the budget for 2016. The market continued to drop in spite of this pragmatic incentive. Global economic conditions had a negative impact on the market. Thus, investors should be vigilant during such times. Observe and correctly evaluate the cause and effect prior to taking rash decisions.

Equity: Alternative avenue for the government

Taxation is not the only mode of increasing revenue. It is suggested that the government could look at equity as a mode of increasing income. Even though Sri Lanka is a welfare state there are several institutions that generate considerable profits. The government could generate income by selling a stake (preferably not more than 10 percent) of these profitable state-owned institutions through the stock market. Differently stated ownership (partial) would transfer to the public. For an example the government could retain 90 percent of profit-making entities and issue 10 percent to the public.

Sing a different tune

State entities’ entering the market is a pragmatic approach that requires much attention.

Listing state intuitions will increase transparency and good governance while curbing corruption. Listing requires the adherence of certain rules that promote a level playing field in the market. As a result it is mandatory to disclose price sensitive information to the market. Further on, listed entities are expected to issue audited financials within five months of the end of the financial year. Quarterly reports are also issued to the public.

Listing is also seen as an ideal buffer against the politicization of these entities. Politicians controlling bureaucrats were a common phenomenon since independence. Such unhealthy practices could be kept well under control by issuing a stake to the public.

Throughout the years the state bureaucracy was criticized for its inefficiency and improper allocation of resources. However by listing in the market, these institutions will be able to employ the services of the private sector that would not only promote efficiency but also provide a new perspective.

It is also important for these companies to issue shares to its employees (similar to the procedure adopted by Sri Lanka Telecom) through a share option scheme. The employees will not only be shareholders of their place of work but also could earn profits by selling the shares in the market.

Sri Lanka is a welfare state and as a result the government has a heavy burden to shoulder. In such situations it is not feasible to maintain non-strategic investments that don’t benefit the public at large. Unfortunately such investments (Waters Edge, Hotel Developers (Hilton),Hyatt Residencies, Lanka Hospitals, Grand Oriental Hotel and Mobitel) were taken over by the government during the previous regime. Perhaps the government could list these entities in order to pave the way for the private sector to take over such institutions. This line of thought was manifested in the national budget for the year 2016.

It is all about the right balance

The effectiveness of this approach will greatly depend on the stake the government intends to hold on to. For an example selling a stake of around 10 percent is seen as a healthy move as the government is left with 90 percent. It is vital for the government to have a considerable stake in these strategic moves. Moving on, key welfare functions (health, education, etc.) should continue to be under the domain of the government. Citizens should not fall prey to political propaganda that overstates the status quo. Efficiency is the key towards growth and it is undoubted that a fine blend of government and private sector will promote efficiency. Nevertheless, the government will have to pay attention to the various technical issues that may come up in order for this initiative to be a success.

Stock market growth

If profitable government institutions (Bank of Ceylon, Peoples Bank, etc.) issue around a 10 percent stake the stock market would be heading for better times. It could increase market capitalization and liquidity. These are key impediments that hinder the growth of the market. State institutions are expected to be secure, thus listing these will be a giant leap in building investor confidence. One would even suggest that listing government entities would increase the investor base.

In conclusion it could be deduced that encouraging profitable state institutions to list would be more appropriate than introducing direct taxes (capital gain tax) when managing public finance

http://www.dailymirror.lk/106801/The-dilemma-of-public-finance-Tradeoff-between-taxation-and-equity#sthash.SYrN8o6q.dpuf

Debt is a burning issue

The previous regime provided impetus towards economic growth by increasing government expenditure through debt financing. As a result, government debt has exceeded manageable limits. According to the latest documents, the country’s total outstanding loans at the end of year 2015 were Rs.8,475 billion, which amounts to 74.9 percent of the gross domestic product (GDP). The country is in a horrendous debt trap of Rs.9.5 trillion.

Even though increasing demand through government expenditure is a widely accepted economic policy centralizing such policies around unsustainable levels of debt is inappropriate. As a result, the country is currently faced with a debt trap.

The way forward

On one hand, the government has to manage the debt trap and on the other hand it has to manage the impact of the global economic slowdown. The current predicament compels the government to take up stringent measures in relation to fiscal and monetary policy. Accordingly, increasing tax revenue becomes a feasible fiscal tool.

Prime Minister Ranil Wickremesinghe adopted the aforesaid approach by making proposals to the parliament to change certain taxes. Principal among these changes is the reintroduction of capital gains tax, increasing the rate of Value Added Tax (VAT), removing certain exemption on VAT and Nation Building Tax (NBT) and thereby widening the tax base.

Historical data reveals that tax revenue as percent of the GDP has not only been below 15 percent but also recorded a declining trend (refer graph 1) since 2006. Further on taxes on income, profits and capital gains (percent of total taxes) has also been relatively low when compared to its counterparts(graph 2). One would argue that the structural deficiencies in tax collection/tax structure and popular politics can be attributed to low tax levels. Employing this fiscal tool is long overdue. Nevertheless, its appropriateness within the current context is questionable.

Capital Gains Tax

It has been proposed to reintroduce tax on capital gains. A capital gains tax is a type of tax levied on capital gains incurred by individuals and corporations. Capital gains are the profits that an investor realizes when he or she sells the capital asset for a price that is higher than the purchase price. An investor can own shares that appreciate every year, but the investor does not incur a capital gains tax on the shares until they are sold. It was proposed to introduce this tax for capital gains generated in the stock market. This could be explained further through an example. Imagine that you purchased 1000 shares at Rs.2 from the market. After one year you sell the share at Rs.3.Then your capital gain will be Rs.1000.According to the proposed amendment a tax will be levied on the capital gain of Rs.1000.

The capital gain tax would have a direct impact on the market. The market has decreased by more than 10 percent for the current year. The current trend is in line with global equity prices that have plunged down drastically. For an example, the Chinese stock market has decreased by 24percent this year. Nevertheless the local equity market has managed to sustain a satisfactory performance in comparison to its counterparts. However, it is reasonable to question if these commendable levels will continue amidst the tax amendment. Investment decision-making is well grounded on expected returns. Tax of this nature would reduce expected returns and investors would be compelled to look at other avenues amidst rising interest rates.

Benjamin Graham in his book ‘The Intelligent Investor’ states that investing in the market is more about emotion than intelligence. Hence, introducing this tax within the current market condition might falter investor confidence and create undue resistance towards equity. Situation might aggravate due to the herd mentality in the market.

Could direct taxes hinder growth?

The country is currently burdened with debt. In such an environment a government is faced with a few options. They could increase tax revenue, encourage FDIs or enter into more debt to repay of the current debt. It is well established that the latter is inappropriate and thereby we are left with the first two options.

Direct taxes (e.g. capital gain tax) reduce the real income of households. This would hamper consumption and thereby reduce aggregate demand in the economy which is a key driver of economic growth. Slowdown in growth will worsen the debt situation.

Ease of doing business, conducive tax structure and political/economic stability will be the manthra to attract FDIs. A tax that hampers profits will definitely compel investors to look at competitors as India, China, Vietnam, etc. The same principle would apply for portfolio investments. The government is indeed faced with a double edged sword. On the one hand it is exploring the opportunities of attracting FDIs and on the other hand might fail to foster a suitable environment for investment. It is rational to postulate the returns on tax revenue in comparison to the loss of foreign investment.

Clearing the air

There are a few decisive factors that would determine the impact of this tax especially in the context of the stock market. The tax structure has not been revealed as yet. The industry is optimistic that it will be between manageable limits. Further on the responsiveness of the capital gains tax to investment decision (in the stock market) is another crucial point to ponder on. It is important to bear in mind that market performance is influenced by many factors. Accordingly capital gain tax is a one factor among a myriad of other vital factors.

It could be postulated that the tax might not have a considerable impact on the market if all other factors are in place. This is clearly manifested in the abolition of the Government levy by the budget for 2016. The market continued to drop in spite of this pragmatic incentive. Global economic conditions had a negative impact on the market. Thus, investors should be vigilant during such times. Observe and correctly evaluate the cause and effect prior to taking rash decisions.

Equity: Alternative avenue for the government

Taxation is not the only mode of increasing revenue. It is suggested that the government could look at equity as a mode of increasing income. Even though Sri Lanka is a welfare state there are several institutions that generate considerable profits. The government could generate income by selling a stake (preferably not more than 10 percent) of these profitable state-owned institutions through the stock market. Differently stated ownership (partial) would transfer to the public. For an example the government could retain 90 percent of profit-making entities and issue 10 percent to the public.

Sing a different tune

State entities’ entering the market is a pragmatic approach that requires much attention.

Listing state intuitions will increase transparency and good governance while curbing corruption. Listing requires the adherence of certain rules that promote a level playing field in the market. As a result it is mandatory to disclose price sensitive information to the market. Further on, listed entities are expected to issue audited financials within five months of the end of the financial year. Quarterly reports are also issued to the public.

Listing is also seen as an ideal buffer against the politicization of these entities. Politicians controlling bureaucrats were a common phenomenon since independence. Such unhealthy practices could be kept well under control by issuing a stake to the public.

Throughout the years the state bureaucracy was criticized for its inefficiency and improper allocation of resources. However by listing in the market, these institutions will be able to employ the services of the private sector that would not only promote efficiency but also provide a new perspective.

It is also important for these companies to issue shares to its employees (similar to the procedure adopted by Sri Lanka Telecom) through a share option scheme. The employees will not only be shareholders of their place of work but also could earn profits by selling the shares in the market.

Sri Lanka is a welfare state and as a result the government has a heavy burden to shoulder. In such situations it is not feasible to maintain non-strategic investments that don’t benefit the public at large. Unfortunately such investments (Waters Edge, Hotel Developers (Hilton),Hyatt Residencies, Lanka Hospitals, Grand Oriental Hotel and Mobitel) were taken over by the government during the previous regime. Perhaps the government could list these entities in order to pave the way for the private sector to take over such institutions. This line of thought was manifested in the national budget for the year 2016.

It is all about the right balance

The effectiveness of this approach will greatly depend on the stake the government intends to hold on to. For an example selling a stake of around 10 percent is seen as a healthy move as the government is left with 90 percent. It is vital for the government to have a considerable stake in these strategic moves. Moving on, key welfare functions (health, education, etc.) should continue to be under the domain of the government. Citizens should not fall prey to political propaganda that overstates the status quo. Efficiency is the key towards growth and it is undoubted that a fine blend of government and private sector will promote efficiency. Nevertheless, the government will have to pay attention to the various technical issues that may come up in order for this initiative to be a success.

Stock market growth

If profitable government institutions (Bank of Ceylon, Peoples Bank, etc.) issue around a 10 percent stake the stock market would be heading for better times. It could increase market capitalization and liquidity. These are key impediments that hinder the growth of the market. State institutions are expected to be secure, thus listing these will be a giant leap in building investor confidence. One would even suggest that listing government entities would increase the investor base.

In conclusion it could be deduced that encouraging profitable state institutions to list would be more appropriate than introducing direct taxes (capital gain tax) when managing public finance

http://www.dailymirror.lk/106801/The-dilemma-of-public-finance-Tradeoff-between-taxation-and-equity#sthash.SYrN8o6q.dpuf